NEW YORK, June 12: Nobody said it out loud. Nobody needed to. The moment the ticker SPCX went live on the Nasdaq Global Select Market this morning, everyone in finance understood what had just happened. The largest initial public offering in the history of capital markets $75 billion raised, $1.77 trillion in valuation locked had finally, officially, landed.

- What $75 Billion Actually Means for the SPCX IPO

- The Three Businesses Inside SPCX Stock

- The Consolidated Numbers the SPCX Prospectus Actually Reveals

- The Governance Structure Every SPCX Investor Must Understand

- What Analysts Are Actually Saying About SPCX Stock

- The Starship Variable: Why SPCX Stock Is Also a Bet on a Rocket That Has Not Yet Flown a Commercial Mission

- The Risk Register for SPCX Stock That the Bull Case Tends to Skip

- What the SPCX IPO Means for Business News and Capital Markets in 2026

Twenty-four years. That is how long SpaceX stayed private while the rest of the world watched, waited, and speculated. Through three Falcon 1 failures that nearly bankrupted the company in 2008. Through the first successful commercial cargo delivery to the International Space Station. Through the moment reusable rocketry went from science fiction to standard operating procedure.

Through the explosive growth of Starlink into a global satellite internet empire with more than ten million subscribers. Through the February 2026 acquisition of xAI Elon Musk’s artificial intelligence company in an all stock deal that CNBC called the largest private merger in the history of any industry. Through all of it, SpaceX stayed private. Until today.

The SPCX IPO is not a business news event. It is a capital markets realignment. And any serious investor who approaches it without understanding the machinery underneath the headline number is flying blind.

What $75 Billion Actually Means for the SPCX IPO

The scale of the SPCX IPO is genuinely difficult to absorb without context. Saudi Aramco’s 2019 debut raised $29.4 billion a figure that included the exercise of its overallotment option and held the record for nearly seven years. SpaceX has more than doubled it in a single afternoon.

According to SpaceX’s S-1 registration statement filed with the SEC on May 20, 2026, the company offered approximately 555.6 million shares of Class A common stock at $135 each, with underwriters granted a 30 day option to purchase up to an additional 83.3 million shares at the IPO price.

The offering is expected to formally close on June 15. Total demand exceeded $250 billion, per Reuters and Bloomberg. Retail orders alone surpassed $100 billion, per Bloomberg. The deal was oversubscribed 3.5 to 4 times before a single share changed hands on a public exchange.

That number 3.5 to 4 times oversubscribed tells you something important about where investor appetite for the SPCX IPO sits right now. This is not the kind of demand you manufacture with a good roadshow. This is the product of two decades of watching a company do things that every credentialed expert said were impossible, and then do them again, cheaper, faster, and at scale.

One structural decision SpaceX made in designing the SPCX IPO deserves particular attention because it has never been done at this size before. The company reserved approximately 30% of its public shares for retail investors individual buyers, not institutions. Standard mega IPO practice reserves 5% to 10% for retail. SpaceX tripled that floor and called it intentional. For the first time, ordinary investors were not fighting for scraps at one of the most anticipated public offerings ever priced.

The Three Businesses Inside SPCX Stock

Here is where the SPCX IPO demands intellectual discipline, because the business you are buying is not one business. It is three, and they are performing in dramatically different ways.

The S-1 prospectus organises SpaceX into three operating segments: Connectivity, which is Starlink; Space, which covers rocket launches and government contracts; and AI, which houses xAI, the Grok models, and the social network X. Understanding each segment separately is the only honest way to evaluate what SPCX stock is actually worth.

Starlink is the engine that funds everything else. The Connectivity segment accounted for $11.4 billion in revenue in 2025 approximately 61% of overall company revenue and it is the only segment currently generating profit. According to the S-1 prospectus, Starlink delivered $4.4 billion in operating income in 2025 at a 39% operating margin, with an adjusted EBITDA margin of 63% and adjusted EBITDA of $7.168 billion.

That margin figure is not a rounding error. Traditional satellite operators average roughly 20%. Starlink has built a network where each additional subscriber adds revenue at near zero marginal cost, and the economics are beginning to compound in exactly the way that frightens incumbents.

Subscriber growth backs the margin story. Per the S-1, Starlink grew from 2.3 million subscribers in 2023 to 4.4 million in 2024 to 8.9 million by year end 2025 a 97% compounded annual growth rate. By February 2026, SpaceX reported the service had surpassed 10 million active customers across 160 countries.

As of March 31, 2026, 10.3 million subscribers were served across 164 countries and territories, supported by approximately 9,600 broadband and mobile satellites in low Earth orbit representing 75% of all active maneuverable satellites on the planet, per the S-1 filing.

The pricing dynamic inside Starlink is also undergoing a deliberate shift. The S-1 disclosed that average revenue per subscriber fell 18% to $81 per month between 2023 and 2025, as SpaceX traded ARPU for global volume and subscriber scale. In May 2026, SpaceX reversed that trend by raising Starlink plan prices by up to $10 per month. That is the monetisation dial turning. It has significant rotations remaining.

The Space segment is a strategic asset, not a profit centre. SpaceX’s launch business and crew services to NASA generated $4 billion in revenue in 2025. The segment ran a $657 million operating loss, almost entirely attributable to Starship development R&D, which consumed nearly $3 billion. That loss is not mismanagement.

It is deliberate investment in the vehicle that will carry the next generation of Starlink satellites, orbital data centres, and eventually Mars infrastructure. SpaceX completed 165 orbital launches in 2025 its sixth consecutive annual launch record and launched more than 80% of all mass to orbit globally. The 500th Falcon 9 mission marked a booster flying for a record 29th consecutive reuse.

Government contract depth here is real and expanding. SpaceX was awarded a contract worth over $4 billion for Golden Dome programme satellites, covering an air moving target indicator system that could field up to 600 satellites, anchoring the government portfolio and providing revenue visibility that purely commercial launch businesses cannot replicate.

The AI segment is the wildcard that changes the risk calculus for SPCX stock entirely. On February 2, 2026, SpaceX acquired Musk’s AI startup xAI in an all stock deal that valued the combined entity at approximately $1.25 trillion SpaceX at $1 trillion and xAI at $250 billion the largest private merger in history by any measure, per CNBC. The deal brought xAI’s data centres, the Grok AI models, and the social network X into the SpaceX corporate structure.

In May 2026, Musk announced that xAI would be fully absorbed and rebranded as SpaceXAI. The AI segment generated $3.2 billion in revenue. It also burned $6.4 billion building COLOSSUS data centres and training Grok. That gap is what converted SpaceX from a cash flow positive business into a net loss entity for 2025, producing an operating loss of $2.6 billion on consolidated revenue of $18.67 billion.

The Consolidated Numbers the SPCX Prospectus Actually Reveals

The SpaceX S-1 gave markets the first official, audited look inside a company that had operated in complete financial privacy for twenty four years. The picture it reveals is of a business that is genuinely extraordinary in parts and genuinely expensive to operate in others.

Consolidated revenue for 2025 came in at $18,674 million. Operating loss was $2,589 million. Adjusted EBITDA which strips out the non cash and one time charges that distort the operating picture was $6,584 million. In the first quarter of 2026, quarterly revenue grew to $4.7 billion, the operating loss reached $1.9 billion, and adjusted EBITDA was $1.1 billion, all per the S-1 filing.

The company has accumulated a total deficit of $41.3 billion since Elon Musk founded it in 2002 with approximately $100 million from his PayPal exit. That figure is not a sign of failure.

It is the price tag on building the world’s most advanced private aerospace and satellite infrastructure from nothing, in an industry where the barriers to entry are measured in physics and capital simultaneously. But investors buying SPCX stock in the open market should understand that number with full clarity.

Elon Musk addressed the rationale for the timing of the SPCX IPO directly. On a JPMorgan Chase investor livestream in the days before the offering, Musk stated that SpaceX had been cash flow positive since around 2015, and that he wanted to take SpaceX public now to raise capital for what he described as “a significant growth phase,” citing plans to put over 100,000 satellites in orbit for communications and to build artificial intelligence data centres in space.

Those are not marketing promises. They are the capital requirements that made a $75 billion raise at a $1.77 trillion valuation the only instrument large enough to fund what comes next.

The Governance Structure Every SPCX Investor Must Understand

No serious analysis of SPCX stock is complete without a plain language description of what buying Class A shares actually gives you and what it does not.

Through Class B shares carrying 10 votes each against one vote for Class A shares available to public investors, Elon Musk holds the voting majority and can determine a majority of the SpaceX board of directors. SpaceX is classified as a Controlled Company under Nasdaq rules and takes advantage of corporate governance exemptions that classification permits.

After the SPCX IPO, Musk will hold 85.1% of combined voting power, per the company’s S-1/A filed with the SEC on June 3, 2026. A 366 day lock up period means he must hold all of his SpaceX shares for one year after the listing.

SpaceX’s own prospectus states the position plainly: “We believe that Mr. Musk’s substantial ownership interest in us provides him with an economic incentive to assist us to be successful.”

What this means for SPCX investors is not ambiguous. You are purchasing economic participation in the SpaceX and Starlink and xAI growth story. You are not purchasing governance power, board representation, or any practical mechanism to influence strategic decisions.

Musk’s priorities, his attention, and his execution across SpaceX, Tesla, and his other ventures will determine outcomes for SPCX shareholders in ways that no investment committee can vote around. That is the trade. It should be accepted with full awareness, not discovered after the fact.

What Analysts Are Actually Saying About SPCX Stock

The professional investment community is split in a way that is unusual even for a mega IPO, and that split itself is instructive.

On the bullish side, New Street Research analysts initiated coverage with a 12-month price target of $165 a 22% upside from the $135 offer price, implying a valuation of $2.3 trillion. Oppenheimer’s Timothy Horan went further, assigning an Outperform rating with a $190 target.

MSCI announced on June 9 that SPCX would be eligible for early inclusion in large IPO indices, with index funds beginning to add the stock on June 13 the second day of trading. With only a roughly 4% public float at launch, that mechanical buying pressure from passive index funds creates structural demand that is independent of any fundamental re-rating. Week one analyst price targets range from $140 to $175.

On the sceptical side, Morningstar values the company at $780 billion less than half the IPO target. Their reasoning is grounded in segment level profitability: only Starlink is currently generating operating profit, while xAI is projected to consume approximately $10 billion in capital in 2026.

At roughly 96 to 110 times trailing revenue, SPCX stock would debut at a multiple higher than Tesla, Palantir, or any major technology company currently trading on a public exchange. That multiple implies sustained exceptional performance across multiple business lines over multiple years. History is not generous to companies that enter public markets at this altitude.

The first public earnings report, expected in November 2026, will be the first real test of whether the narrative justifies the number. Until then, SPCX stock will trade on sentiment, index flows, and Starlink subscriber data not on a quarterly earnings cadence that public market investors can lean against.

The Starship Variable: Why SPCX Stock Is Also a Bet on a Rocket That Has Not Yet Flown a Commercial Mission

Every valuation model for SPCX stock eventually leads back to the same assumption: that Starship works, scales, and transforms the economics of access to space in the way SpaceX has projected.

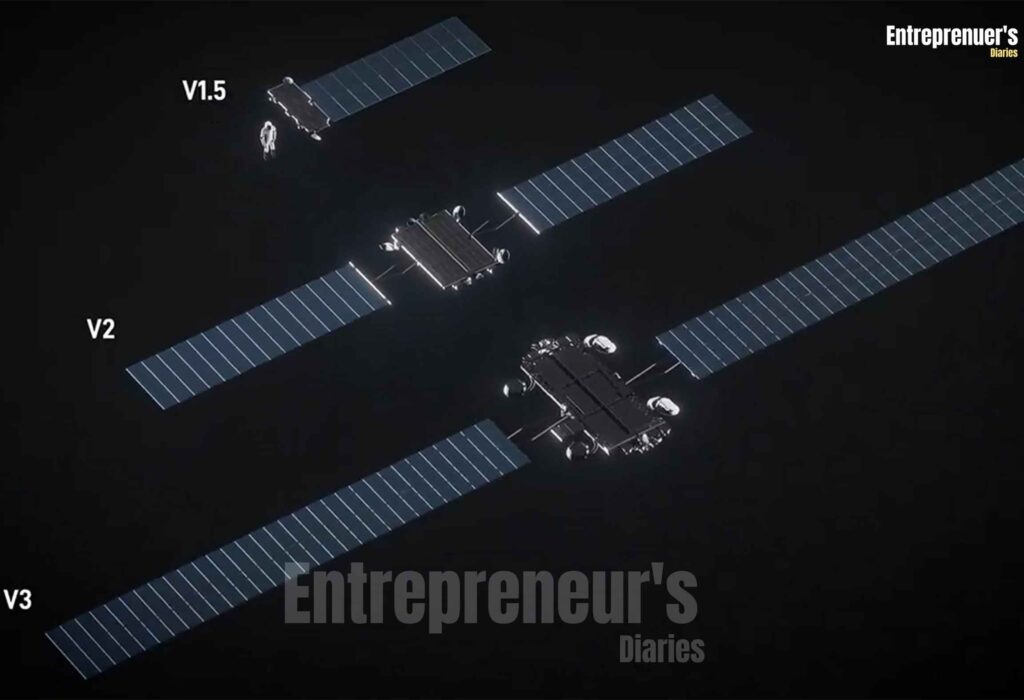

The stakes around Starship for the SPCX IPO are not speculative in the way early stage bets are speculative. SpaceX has conducted eleven Starship test flights. A twelfth is scheduled, and the first productive payload launch is expected in the second half of 2026. SpaceX’s S-1 confirms that V3 satellites each carrying significantly greater capacity than current generation hardware are scheduled to begin deployment on Starship in the second half of 2026.

SpaceX plans to begin launching a new generation of larger V3 Starlink satellites using Starship, with Starship’s payload capacity able to carry approximately 50 of the bigger V3 satellites per launch versus the handful Falcon 9 can manage the operational reason the financial projections for Starlink’s 2027 and 2028 revenue trajectory are as aggressive as they are.

Any delay in Starship’s commercial certification would slow the V3 satellite rollout, the mobile expansion, and the orbital AI compute programme. The warning is not hypothetical it is the risk factor SpaceX’s own S-1 identifies as the primary operational risk. Investors buying SPCX stock are implicitly pricing in a timeline that leaves very little runway for execution stumbles.

The Risk Register for SPCX Stock That the Bull Case Tends to Skip

The case for SPCX stock has been made loudly and repeatedly across Wall Street, and the operational evidence supporting it is genuine. Starlink’s subscriber growth, its margin profile, and SpaceX’s structural dominance in global launch are real, documented, and financially material. The risk case has received considerably less air time, and that asymmetry should make experienced investors cautious.

Valuation compression is the most immediate and least dramatic risk. At 96 to 110 times trailing revenue, SPCX stock enters public markets at a multiple that has never been sustained by any large-cap company at scale. Multiples this elevated compress over time as companies mature, even when the underlying business continues to grow.

Saudi Aramco, the previous IPO record holder, traded below its own IPO price for years after listing. Being the largest IPO in history is not a performance guarantee. It is a very high baseline against which all future results will be measured.

The xAI cost trajectory represents the second major risk embedded in SPCX stock. The AI segment burned $6.4 billion in 2025 and is projected to continue consuming substantial capital through 2026 and beyond as SpaceX builds orbital data centre infrastructure.

Revenue from this segment has not demonstrated the scale necessary to justify its cost base, and the projections for when it will are based on assumptions about Grok adoption and enterprise AI compute demand that remain to be validated in the market.

Governance concentration creates a key-person dependency that has no parallel in the large-cap equity universe. Musk’s track record at SpaceX is extraordinary and well-documented. His track record of divided attention during his involvement with DOGE in 2025, Tesla’s share price and profitability both deteriorated materially is also documented and should be priced in honestly.

What the SPCX IPO Means for Business News and Capital Markets in 2026

The SPCX IPO does not exist in isolation, and understanding its broader significance is part of what positions serious investors correctly for the rest of 2026.

SpaceX is raising more money in this single offering than all U.S. IPOs combined in both 2024 and 2025. The 2026 IPO market entered the year with 71 offerings raising $35.7 billion through early June. SpaceX has more than doubled that figure in a single transaction.

The market infrastructure required to absorb a $75 billion offering the 21-bank syndicate led by Morgan Stanley, Goldman Sachs, JPMorgan, Bank of America, and Citigroup represents a mobilisation of Wall Street capacity not seen since the dot-com era, and executed this time with financial discipline that the dot-com era largely lacked.

Anthropic and OpenAI are both laying groundwork for potential public offerings, and the successful execution of the SPCX IPO opens the door to a wave of AI-era listings that have been waiting for exactly this signal to proceed.

For entrepreneurs and investors watching from outside the aerospace sector, the SPCX IPO carries a message that matters well beyond the space industry. It confirms that capital markets can accommodate companies built on twenty-year time horizons, driven by founders with total operational control, pursuing markets that did not exist when the company was founded. That is not a lesson the market teaches often. When it does, the implications are worth studying carefully.

The honest read on SPCX stock as it begins trading today: it is simultaneously one of the most defensible businesses in the world on unit economics, and one of the most demanding valuations in the history of public markets. Those two things are both true at once, and how that tension resolves over the next twelve months will define SPCX stock’s story for years.

The investors who spent the last decade building exposure to SpaceX at earlier valuations are sitting comfortably today. The ones now buying at $1.77 trillion need to be certain they are investing in an execution story, not paying for one that has already been priced.

Connect With Us On Social Media [ Facebook | Instagram | Twitter | LinkedIn ] To Get Real-Time Updates On The Market. Entrepreneurs’ Diaries Is Now Available On Telegram. Join Our Telegram Channel To Get Instant Updates.

Isabella is a global business journalist and former McKinsey analyst from Brazil. She brings sharp insights on economic shifts, policies, and founder journeys from around the world.

Tokyo-based CFA translating global markets into clear insights for modern entrepreneurs.