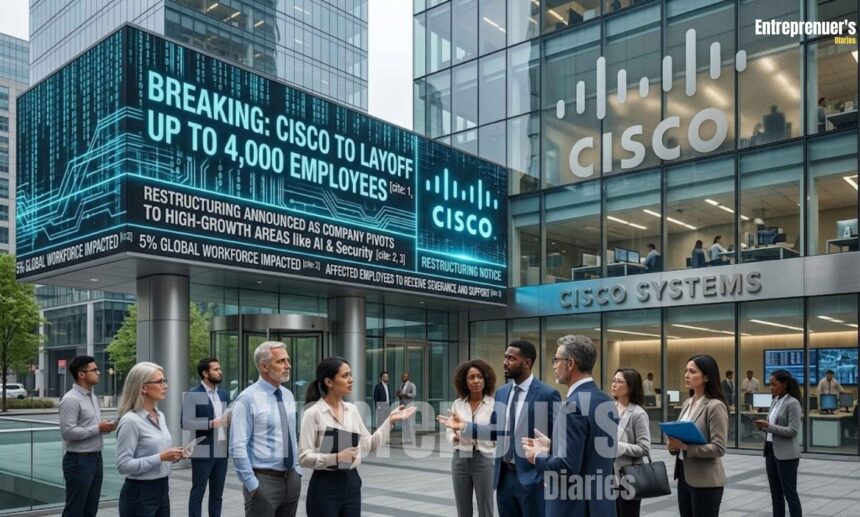

San Jose, May 15: Wednesday was a tough day to be a Cisco employee scrolling through the company newsfeed. The San Jose networking giant confirmed it would cut approximately 4,000 positions, around 5% of its global workforce, while simultaneously telling Wall Street that business has never looked more promising. The contradiction is jarring until you understand the game Cisco is playing. Shares climbed in after-hours trading. The market got the memo.

This is the second time in under two years that Cisco has swung the axe at this scale. Back in February 2024, the company parted ways with roughly 4,250 people as it worked through the digestion of its $28 billion Splunk acquisition. That round was framed as integration math. Messy, but understandable. This one is something else. This is Chief Executive Chuck Robbins telling the world, in the plainest possible terms, that the Cisco he inherited in 2015 and the Cisco he is building for 2030 require fundamentally different human architectures.

The Cisco Layoffs 2026 Strategy: Leaner, Not Smaller in Ambition

There is a version of Cisco that most people still carry in their heads. The one that built the plumbing of the internet. Routers in every server room, switches in every enterprise closet, the indispensable company behind the infrastructure nobody thought about until it stopped working. That business still exists. It still generates serious revenue. But it has been growing like a tree that has hit the ceiling, and anyone who has watched Cisco closely over the past decade saw this reckoning coming.

Cloud providers stopped buying commodity networking hardware and started building their own. Software-defined networking chipped away at the premium Cisco charged for proprietary gear. The margins that once made the company one of the most profitable in technology began to compress. Robbins has spent the better part of his tenure pulling the company out of that gravity, steering it toward software subscriptions, cybersecurity, and now the kind of AI-era infrastructure that has enterprise IT departments opening their wallets again.

The 4,000 Cisco layoffs announced this week are the price of finishing that transformation. As Robbins put it in a statement accompanying the earnings release, reported by Reuters and Bloomberg: “We are continuing to execute on our strategy to align our investments in our highest priority areas, particularly in AI infrastructure, security, and our platform approach.”

The company has not yet said which teams or geographies take the hardest hit. What it did say is that the restructuring will carry charges of between $700 million and $800 million, spread across the fourth quarter of fiscal 2026 and into fiscal 2027. Severance, real estate wind-downs, the standard accounting of human displacement.

The Numbers Behind the Cisco Layoffs 2026

Strip away the strategic language and what you have is a company that had a decent quarter. Cisco’s fiscal third-quarter 2026 revenue came in at approximately $14.1 billion, ahead of analyst expectations and up on the prior year. The Splunk integration, once a source of Wall Street skepticism given the price tag, is finally showing up in the numbers. The cybersecurity and observability segment that Splunk anchors contributed meaningfully to the top line. Annualized recurring revenue, the metric Cisco most wants investors watching, kept moving in the right direction.

Off the back of those results, the company bumped its full-year fiscal 2026 revenue guidance upward by several hundred million dollars at both ends of the range. That is not a defensive move. That is management telling analysts they see something real in the pipeline.

What they see is AI. Specifically, the extraordinary appetite among hyperscale cloud providers and large enterprises for the high-speed networking infrastructure that AI clusters demand. Cisco has been quietly, and sometimes not so quietly, positioning its data center switching portfolio and high-speed Ethernet products as the backbone of choice for AI training and inference buildouts. According to Reuters, it has been closing meaningful deals in that space, competing against InfiniBand-based alternatives in a market that barely existed three years ago.

Cisco entered fiscal 2026 cautiously. Enterprise IT budgets had been clenched for much of 2025 as customers worked through technology they had already bought and were not yet using. That inventory overhang suppressed orders across the networking sector. The raised forecast is a signal that the overhang is clearing, and that the AI infrastructure cycle is real enough to replace it.

Why Tech Giants Keep Cutting Jobs While Revenues Rise

Look, this pattern has repeated often enough now that it deserves a clear-eyed explanation rather than fresh outrage each time it surfaces. Microsoft did it. Meta did it. Alphabet did it. Amazon did it. Cut thousands while reporting strong or improving results, and watched the stock go up. To people who lost their jobs, that feels obscene. To investors, it feels like discipline. Both reactions are legitimate.

The pandemic hiring bubble is the original sin. Between 2020 and 2022, technology companies hired with a recklessness the market only punished after the fact. Cisco was no exception. It also absorbed thousands of Splunk employees through acquisition. The headcount it carries today reflects a bet on a growth trajectory that never materialized the way the spreadsheets once suggested it would.

Then there is the productivity question, which is harder to argue with. Cisco’s own engineers are working with AI tools that let smaller teams ship faster. Sales workflows that required a certain number of humans 18 months ago require fewer today. The math of labor in technology is being rewritten in real time, and every CFO at every major firm is running the same calculations. It is uncomfortable, but it is not mysterious.

And then there is the investor pressure. Technology companies trade at premium multiples on the promise of operating leverage: the ability to grow revenue faster than costs. Any company that lets its cost base expand in line with revenue is, in investors’ eyes, leaving margin on the table. The pairing of layoffs with raised guidance is a very deliberate communication: management is in control of both sides of the ledger.

None of which changes the reality for the 4,000 people on the wrong side of this announcement. These are engineers, product managers, salespeople, operations staff. People who organized their lives around a company that has been a fixture of enterprise technology for three decades. The restructuring charge is a line item. Their disruption is not.

Chuck Robbins and the Long Game

Robbins is a careful man. Not flashy, not the kind of CEO who courts controversy or makes sweeping pronouncements about changing the world. He has led Cisco through a decade of genuine structural upheaval without the company losing its footing, and that is harder than it looks from the outside.

The Splunk deal was his biggest gamble. At $28 billion it was the kind of acquisition that ends careers when it goes wrong. The initial market reaction was lukewarm. Some analysts thought he overpaid, and they made that case loudly. The integration was messy. But Robbins held his ground, and the strategic logic is now visible: Splunk’s security operations and data analytics capabilities are the connective tissue of the unified security platform Cisco is building, competing for enterprise security budgets that are growing faster than almost any other segment in corporate IT.

According to Gartner, global enterprise cybersecurity spending is on course to exceed $300 billion in 2026. That market is being driven by a threat environment that keeps worsening and by a regulatory tide, from the EU’s NIS2 directive to the SEC’s updated disclosure requirements in the United States, that is forcing boards to take security spending seriously in a way they never quite managed before. Cisco is in that market now in a way it was not before Splunk.

The AI networking angle is where Robbins has placed the second big chip. Bank of America analysts, as reported by Bloomberg, have estimated that AI infrastructure buildouts could add tens of billions of dollars in incremental networking spend over the next three to five years. That is not a niche opportunity. That is a market that could reset Cisco’s growth trajectory if it captures a defensible share.

By cutting now and cutting decisively, Robbins is trying to enter that spending cycle lean. A company carrying excess headcount into a growth phase gets slower and more expensive at exactly the wrong moment. The workforce reduction, viewed through that lens, is preparation rather than retreat.

The Competitive Landscape Is Not Waiting

That said, nobody is holding the door open for Cisco. Arista Networks has built a commanding position in AI data center networking, earning customer trust in segments where Cisco once operated with near-monopoly comfort. Arista is not a scrappy startup anymore. It is a serious, focused rival with a product portfolio specifically engineered for the AI infrastructure era, and it has been taking share.

Juniper Networks, absorbed into Hewlett Packard Enterprise, brings a different threat: scale and a broadened set of enterprise relationships. And the hyperscale cloud providers, Amazon, Microsoft, Google, Meta, remain simultaneously Cisco’s best customers and its most dangerous long-term risk. Each of them is investing steadily in internal networking technology designed, over time, to reduce dependency on outside vendors.

The security market is its own brutal arena. Palo Alto Networks, CrowdStrike, and Fortinet are not standing still. Each has built an ecosystem that becomes harder to displace every year. Cisco’s argument to enterprise customers is consolidation: one vendor for networking and security, fewer integrations, less operational complexity. It is a compelling pitch to IT teams exhausted by sprawling vendor landscapes. Winning that pitch repeatedly, at scale, is an entirely different thing from having it resonate in a boardroom.

Frankly, that is the real test Robbins faces. Not whether the strategy is correct, because most serious analysts think it is. The test is whether the organization he is rebuilding can execute at the speed the market demands. Integration, product development, sales transformation, cost discipline: all simultaneously, across a company of more than 80,000 people. That combination has broken better strategies than this one.

What This Means for the Technology Sector

Cisco’s announcement does not exist in isolation. It is the latest chapter in a story running across the entire technology industry: the companies that benefited most from the digital expansion of the past decade are restructuring for an era defined less by headcount growth and more by output per person.

The 4,000 Cisco layoffs are a conviction move, not a distress signal. The raised revenue guidance on the same day makes that distinction clear. Companies cutting from weakness do not raise their forecasts.

For anyone working in enterprise technology, the broader signal is uncomfortable but legible. The organizations investing most heavily in AI are also the ones most aggressively reducing the roles that AI is making redundant or marginal. That is not a new story. It is the industrial pattern of every major technology transition in modern history, just running at a pace none of the previous ones matched.

Whether Cisco’s bet pays off will be settled not in earnings calls but in data centers, in the bowels of cloud infrastructure, in the security operations centers of the Global 2000. The company has placed its chips on AI networking and unified security. It has restructured to carry that bet as efficiently as possible. And it has told the market, in no uncertain terms, that it believes the next phase is worth the price of this one.

Right now, Robbins looks like he knows exactly what he is doing. He has been right before when the skeptics were loudest. The next few quarters will say whether this time is the same.

Connect With Us On Social Media [ Facebook | Instagram | Twitter | LinkedIn ] To Get Real-Time Updates On The Market. Entrepreneurs’ Diaries Is Now Available On Telegram. Join Our Telegram Channel To Get Instant Updates.

Isabella is a global business journalist and former McKinsey analyst from Brazil. She brings sharp insights on economic shifts, policies, and founder journeys from around the world.

Tokyo-based CFA translating global markets into clear insights for modern entrepreneurs.