New York, June 13, 2026: The Paramount Warner Bros merger just cleared its biggest hurdle and it wasn’t even close. On the afternoon of Friday, June 12, 2026, the U.S. Department of Justice’s Antitrust Division issued a formal press release from the Office of Public Affairs, published on the official government website of the United States Department of Justice. Eight months. Two million documents. Over 80 parties examined.

- THE INVESTIGATION: EIGHT MONTHS, TWO MILLION DOCUMENTS

- THREE MARKETS, THREE VERDICTS

- THE DEAL STRUCTURE: WHAT THE OFFICIAL FILINGS SAY

- WHAT BOTH CEOs SAID ON THE RECORD

- THE CONTENT AND MARKET COMMITMENTS: WHAT WAS FILED WITH THE SEC

- WHAT THE DOJ REJECTED AND WHY IT MATTERS

- WHAT REMAINS UNRESOLVED

- THE BOTTOM LINE: WHAT THE PARAMOUNT WARNER BROS MERGER ACTUALLY MEANS

The outcome was as clean as it gets in antitrust law. The Division determined, based on the evidence received in its investigation, that the transaction is not likely to result in harm to competition or American consumers including with respect to streaming video on demand, linear television, and studio development, production, or distribution of films for theatrical release. No divestitures. No behavioral remedies. No concessions of any kind.

For investors and media industry watchers, that single determination from the Justice Department changes the trajectory of the most closely watched corporate takeover in American entertainment since AT&T’s acquisition of Time Warner in 2018.

THE INVESTIGATION: EIGHT MONTHS, TWO MILLION DOCUMENTS

This was not a rubber stamp review. The Division conducted a rigorous eight month investigation led entirely by the Division’s career staff a point the agency itself emphasized in its official statement, distancing the conclusion from any suggestion of political influence.

Over the course of that investigation, the Division received from the parties over two million documents from over 80 custodians, substantial productions of data, as well as extensive documents, data, and advocacy from third parties across the media and entertainment ecosystem. That is the scale of a full scale antitrust trial preparation, not a routine clearance process.

The Division’s official statement also confirmed that State Attorney General offices participated in the investigation by virtue of the parties’ voluntary waivers of confidentiality. This arrangement allowed the Division and the states to share information with each other, and for state offices to attend and participate directly in the Division’s depositions. That detail is significant: the very state authorities now threatening to challenge the deal were inside the room during the federal investigation.

The Division reviewed something even more unusual a competing bid. In December 2025, Netflix had entered into an agreement to acquire WBD. Paramount subsequently submitted an all cash tender offer. The Division reviewed both proposals. As a consequence of the competitive bidding process between Netflix and Paramount to acquire Warner Bros., the review of competitive impacts began prior to Paramount reaching a definitive agreement with WBD. The DOJ, in its own words, benefited from the comparative perspectives and contrasting visions presented in these competing proposals on the evolving media and entertainment landscape and the strategic value of WBD.

The agency did not analyze this deal in a vacuum. It effectively ran a parallel assessment of two competing industrial visions for the future of American media and found the Paramount path was the cleaner one competitively.

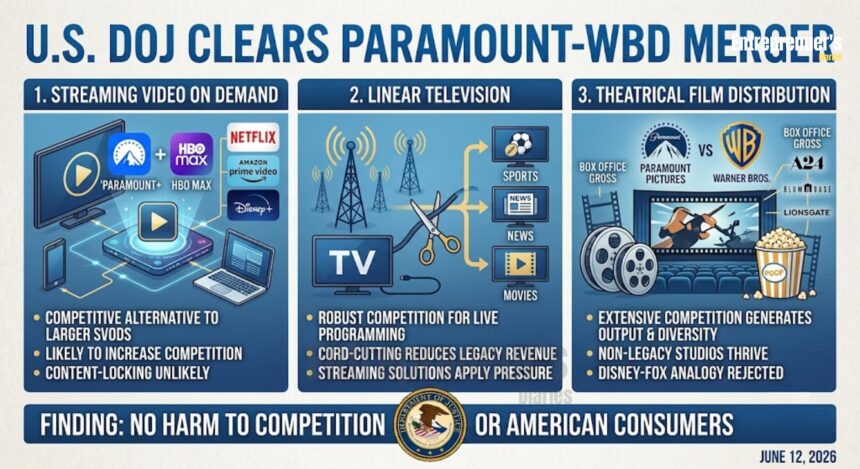

THREE MARKETS, THREE VERDICTS

The DOJ’s official statement addressed competition in three distinct markets. Each finding is independent. Taken together, they constitute a comprehensive regulatory clearance across the full scope of the transaction.

Streaming Video On Demand

The Division found that post merger, competition in SVOD is not likely to be harmed. To the contrary, per the official statement, the combined firm is likely to increase competition by offering consumers a more robust competitive alternative to the larger SVOD offerings.

The Division also addressed the content locking concern that had circulated among critics the theory that the combined company might restrict its IP to its own platforms rather than licensing broadly across the industry. It rejected that theory outright, finding that such an outcome appears unlikely given the parties’ historical practices of broadly licensing content, and that no evidence was found to suggest that Paramount’s historical practice or incentive to do so would end following the transaction.

On social media platforms, the DOJ issued a precise legal clarification: non SVOD video alternatives such as YouTube, TikTok, or other social media products do not appear to be competitive substitutes under well established antitrust legal precedents, although they compete broadly for consumer attention. Arguments that YouTube or TikTok diminish the competitive significance of a merged streaming entity were rejected on the evidentiary record.

Linear Television

The Division concluded the proposed acquisition is not likely to harm competition for linear television, citing the robust competitive landscape for live programming.

The DOJ’s statement acknowledged the structural reality: cord cutting has substantially reduced revenue to both linear network owners and traditional distributors. Streaming solutions now compete aggressively for live programming including premier sports rights, news, and political commentary putting increasing competitive pressure on legacy linear networks to secure live programming at higher costs. The competitive pressure, the Division found, runs against the combined entity, not in its favor.

Theatrical Film Distribution

This was the most politically charged arena, given vocal opposition from Hollywood talent guilds, the Teamsters, and California’s Attorney General all of whom argued the merger would reduce output and harm workers.

The Division found, based on substantial evidence, that the transaction is not likely to harm competition in studio development, production, or distribution of films for theatrical release. The evidence shows extensive competition within the industry, which has generated greater output and diversity of film offerings, and is likely to continue unabated.

Notably, the Division said that even since the transaction was announced, competition for theatrical production and distribution has increased. It cited specific box office successes from non legacy studios as evidence of a genuinely competitive market: Amazon MGM’s Project Hail Mary, A24’s Backrooms, Lionsgate’s Michael, and Blumhouse’s Obsession. These were not rhetorical examples. They were cited in the official statement as proof that a studio’s legacy no longer determines whether it can succeed in the domestic box office.

The Division also directly rejected the Disney Fox deal as a comparable benchmark. Its official statement characterized reliance on that comparison as fatally flawed, noting that the Disney Fox transaction closed a year before the COVID pandemic began, which drove dramatic changes in studio output and audience content consumption patterns. The two situations, the DOJ concluded, are not analogous.

THE DEAL STRUCTURE: WHAT THE OFFICIAL FILINGS SAY

The financial architecture of this transaction is a matter of public record, contained in an 8-K filing submitted to the U.S. Securities and Exchange Commission by Warner Bros. Discovery, Inc. on February 27, 2026.

Paramount will acquire 100 percent of WBD for $31 per share in cash, plus the ticking fee, valuing WBD at $81 billion in equity value and $110 billion in enterprise value. The transaction has been unanimously approved by the boards of directors of both companies.

Paramount expects the acquisition to yield over $6 billion in synergies. These are driven by technology integration including migrating the combined company to a single enterprise resource planning system and consolidating streaming technology stacks alongside corporate wide efficiencies including procurement savings, optimization of the combined real estate footprint, and broader operational streamlining.

On a fully synergized basis, this values WBD at 7.5 times 2026 EBITDA. At closing, Paramount expects net debt to EBITDA of 4.3 times on a synergized basis, with a stated path to investment grade credit metrics within three years of closing.

The transaction is funded by $47 billion in equity, fully backed by the Ellison Family and RedBird Capital Partners. In addition, the transaction is backed by $54 billion in debt commitments from Bank of America, Citigroup, and Apollo including $15 billion to backstop WBD’s existing bridge facility and $39 billion of incremental new debt.

In the event the transaction has not closed by September 30, 2026, WBD shareholders will receive a $0.25 per share ticking fee for each quarter, measured daily, until closing. The deal also carries a $7 billion regulatory termination fee. That September 30 deadline is not symbolic. It is the financial pressure valve that has been running since the day the deal was announced.

WHAT BOTH CEOs SAID ON THE RECORD

Both David Ellison and David Zaslav made formal public statements at the time of the merger announcement on February 27, 2026. Those statements were filed with the U.S. Securities and Exchange Commission and are part of the official public record.

David Ellison, Chairman and CEO of Paramount, stated: “From the very beginning, our pursuit of Warner Bros. Discovery has been guided by a clear purpose: to honor the legacy of two iconic companies while accelerating our vision of building a next generation media and entertainment company. By bringing together these world class studios, our complementary streaming platforms, and the extraordinary talent behind them, we will create even greater value for audiences, partners and shareholders.”

David Zaslav, President and CEO of Warner Bros. Discovery, stated: “I’m very pleased with the outcome we achieved for WBD shareholders and the entertainment industry. Our guiding principle throughout this process has been to secure a transaction that maximizes the value of our iconic assets and our century old studio while delivering as much certainty as possible for our investors. We look forward to working with Paramount to complete this historic transaction.”

Both statements were made in the context of announcing a definitive merger agreement not a letter of intent, not a tender offer, but a signed, board approved agreement. That distinction matters when evaluating the credibility of the commitments attached to it.

THE CONTENT AND MARKET COMMITMENTS: WHAT WAS FILED WITH THE SEC

Beyond financial terms, the companies made specific operational commitments in the official SEC filing that form part of the legal structure of the transaction. The combined company committed to producing a minimum of 30 theatrical films annually 15 per studio delivering what the filing described as exceptional entertainment to audiences and driving long term job growth across the film and creative industries.

Every film will receive a full theatrical release, with a minimum 45-day window globally before becoming available on paid video on demand, with the intention of 60 to 90 days or more for the most successful releases.

Both studios will continue to support a vibrant third party ecosystem by licensing their films and shows across their own and third party platforms, while remaining active buyers of content from third party studios and independent producers.

The combined company will own a film library of more than 15,000 titles and thousands of hours of television programming. It will be home to some of the world’s most commercially powerful franchises, including Harry Potter, Mission Impossible, Lord of the Rings, Game of Thrones, the DC Universe, Teenage Mutant Ninja Turtles, Transformers, Star Trek and SpongeBob SquarePants, as stated in the SEC filing.

The merged company will hold one of the industry’s most competitive portfolios of sports rights, including the NFL, Olympics, UFC, PGA Tour, NHL, Big Ten and Big 12 Football, NCAA College Basketball, and Champions League all distributable collectively across its platforms.

WHAT THE DOJ REJECTED AND WHY IT MATTERS

The Division directly addressed and dismissed two theories of harm that critics had spent months publicly advancing. The first was the theatrical harm theory the argument that this merger would reduce film output just as the Disney Fox deal allegedly did. The DOJ did not merely disagree with that comparison. It called it fatally flawed due to the pandemic, and backed its rejection with current market data showing output has actually increased since the deal was announced.

The second was the labor harm theory the argument that consolidation would lead to fewer jobs for writers, directors, actors, and crew. The Teamsters Union had urged the DOJ to block the deal unless Paramount agreed to substantial and enforceable safeguards against job cuts, as reported by Variety. The Division took the concern seriously and then formally dismissed it. The official statement concluded that demand for creative workers and labor is correlated with the parties’ incentives to maintain or expand output, and that the expressed labor concerns do not raise actionable antitrust concerns.

That is the DOJ, on the official record, telling Hollywood that the legal framework for antitrust does not extend to speculative employment outcomes in a market where output is currently growing.

The Division closed its formal statement with precise language: the film and television industry is highly dynamic, and the proposed transaction is not likely to harm competition or American consumers.

WHAT REMAINS UNRESOLVED

The DOJ clearance does not complete the transaction. Several regulatory processes remain open.0 The European Commission had listed July 7, 2026 as a tentative deadline for its review, as reported by Courthouse News Service. The UK’s Competition and Markets Authority is targeting an initial decision by early August, per the same reporting. If European or British regulators impose structural conditions asset sales, licensing requirements, or distribution mandates those would carry direct commercial implications for the combined company’s international operations.

California Attorney General Rob Bonta posted publicly on June 12, 2026 that the merger of Warner Bros and Paramount remains under investigation by his office. State attorneys general retain independent antitrust authority. A state level legal challenge, even one unlikely to succeed on the merits, carries the practical capacity to delay closing and potentially push the transaction past the September 30 ticking fee threshold.

The Federal Communications Commission has also not yet made a determination on foreign investment elements of the transaction. In April, Paramount asked the FCC to approve the foreign investments backing the acquisition. U.S. senators raised concerns about the participation of Middle Eastern sovereign wealth funds and Chinese companies, as reported by The Globe and Mail. That review remains open. The DOJ clearance is the most important regulatory door that has opened. It is not the last.

THE BOTTOM LINE: WHAT THE PARAMOUNT WARNER BROS MERGER ACTUALLY MEANS

Here is what most business news coverage will miss and what investors, entrepreneurs, and anyone who operates in or around the media industry should actually absorb.

The DOJ did not simply say this merger is legal. It said it is actively pro competitive. That is a materially different conclusion. After reviewing over two million documents, deposing senior executives at both companies, and examining the industry through the lens of two competing bids, the Division concluded that the streaming market has become competitive enough that two Hollywood studios combining does not tip the balance against consumers it corrects it.

That conclusion rests on a structural reality that is now part of the official U.S. regulatory record: Netflix, Amazon, Apple, A24, Blumhouse, and a new generation of independently financed studios have permanently changed what market power means in entertainment. The entry barriers that once defined Hollywood’s competitive moat studio infrastructure, distribution networks, decades of IP are no longer sufficient to sustain a legal presumption of harm when those same studios sit below Netflix, Amazon, and Apple in subscriber count and balance sheet strength.

This is the DOJ formally acknowledging, in an antitrust context, that the old Hollywood oligopoly has already been disrupted by technology and capital. The merger is not creating a monopoly. It is a defensive consolidation in a market that has already been transformed from outside.

For investors, the absence of any required divestitures is the single most value preserving outcome of all possible scenarios. The $6 billion synergy target filed with the SEC and the engine of the deal’s return thesis is fully intact. Had the DOJ required asset sales, that figure would have been reduced significantly, and the 7.5 times synergized EBITDA valuation multiple would have been repriced. It was not.

For entrepreneurs building in the content, technology, or distribution layers of this ecosystem, the implications are equally real. A combined entity with 15,000 film titles, the NFL, the UFC, HBO, CNN, CBS, Paramount+, HBO Max, and Pluto TV under a single ownership structure with stated commitments to licensing broadly and buying third party content is a large and well capitalized client, partner, and competitor simultaneously. That changes the commercial calculus across the independent studio, production technology, and ad tech sectors immediately.

The real contest now moves to Sacramento, Brussels, and London. California’s AG has the political motivation and independent legal authority to file a challenge. Europe may extract conditions the DOJ would not. And every day past September 30 costs money.

But on June 12, 2026, the most powerful antitrust authority in the United States reviewed this $110 billion deal for eight months, examined two competing bids, produced two million documents, deposed senior executives, invited the states into the room and said: proceed.

That verdict does not guarantee a smooth closing. But it does confirm something more durable: the U.S. government’s official position is that this merger strengthens competition in American media. Anyone arguing otherwise is now arguing against the evidentiary record of a federal investigation. In an industry that has spent a decade being told it is losing, that is a significant thing to have on the record.

Connect With Us On Social Media [ Facebook | Instagram | Twitter | LinkedIn ] To Get Real-Time Updates On The Market. Entrepreneurs’ Diaries Is Now Available On Telegram. Join Our Telegram Channel To Get Instant Updates.

Isabella is a global business journalist and former McKinsey analyst from Brazil. She brings sharp insights on economic shifts, policies, and founder journeys from around the world.

Tokyo-based CFA translating global markets into clear insights for modern entrepreneurs.